A complete, product-neutral guide to understanding Inbound and Outbound investment routes from GIFT IFSC – for NRIs, Indian residents, and global investors.

What is GIFT City & IFSC?

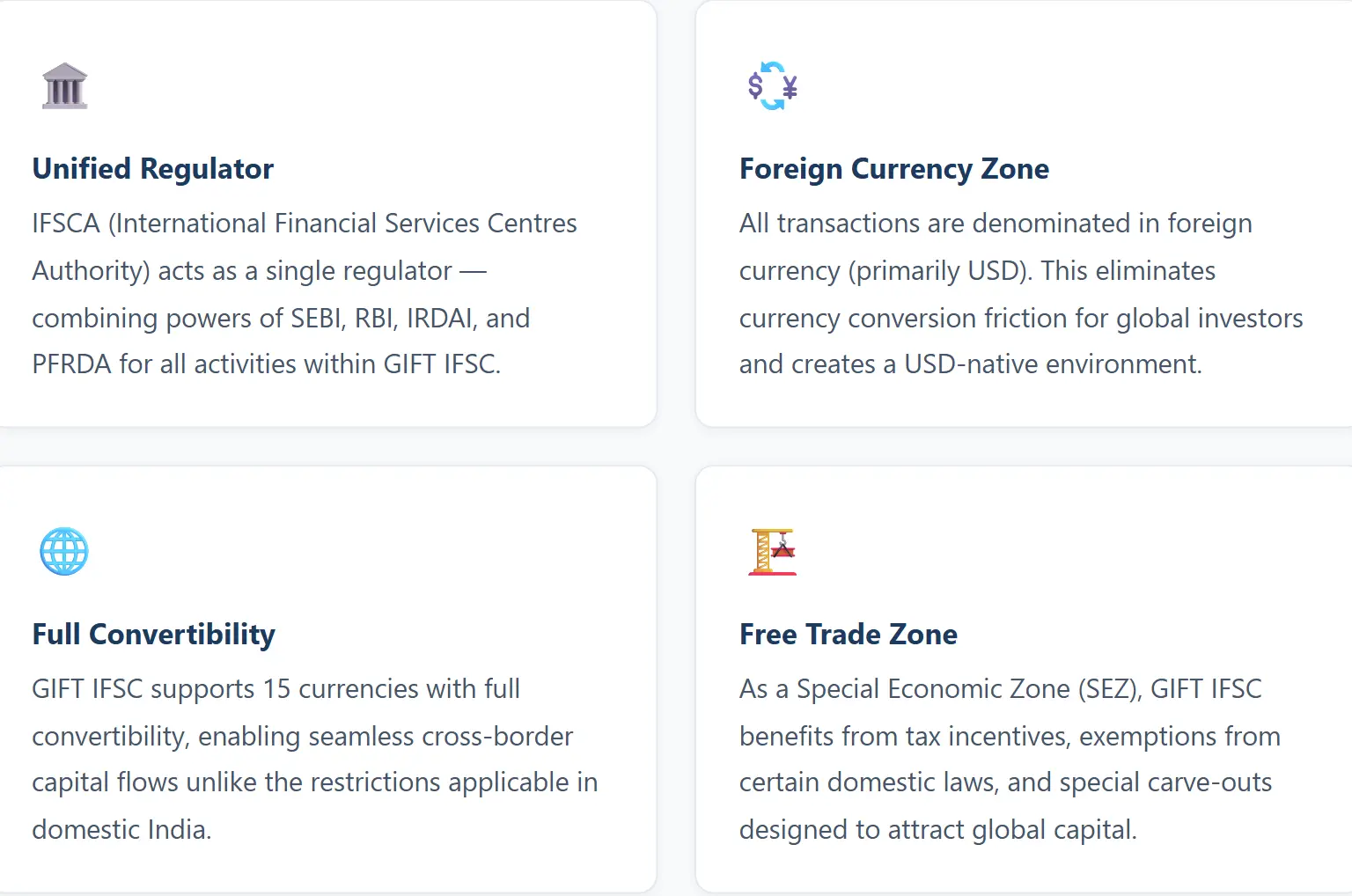

GIFT City – short for Gujarat International Finance Tec-City – is India’s first and only approved International Financial Services Centre (IFSC). Located in Gandhinagar, Gujarat, it is a purpose-built financial district designed to compete with global hubs like Singapore, Dubai’s DIFC, and London’s Canary Wharf.

Think of it as an “onshore-offshore” zone. Legally, under FEMA (Foreign Exchange Management Act), entities operating within GIFT IFSC are treated as non-residents – even though they are physically located in India. This gives the entire ecosystem the regulatory and tax characteristics of an offshore jurisdiction, while still operating under Indian law and the oversight of a single unified regulator.

Key Fact: As of August 2025, total banking assets in GIFT IFSC have surpassed $94 billion, and monthly trading turnover on IFSC exchanges has exceeded $100 billion. Over 200 AIFs are registered with committed capital of over $15 billion. The ecosystem is growing rapidly.

Why Does GIFT City Matter for Investors?

For decades, cross-border investing from India was fragmented, expensive, and compliance-heavy. Indian residents wanting global exposure had limited options – offshore brokerage accounts, limited mutual fund windows, or complex ODI routes. NRIs wanting Indian exposure had to navigate multiple regulators, TDS complications, and repatriation paperwork.

GIFT City changes the calculus fundamentally. It creates a single, regulated gateway for two-directional capital flows:

🔵 Inbound Flow

- Foreign / NRI capital into India

- Access India’s growth story

- USD-denominated, no INR conversion needed

- Simplified KYC – no Indian PAN required for NRIs in many cases

- Full repatriation in foreign currency

🟢 Outbound Flow

- Indian capital into global markets

- Access US, European, global equities

- Via LRS (up to $250,000/year for residents)

- OPI route for corporates and family offices

- Tax paid at fund level – simpler compliance

The beauty of GIFT City is that it serves both these flows under one regulatory roof, creating an efficient two-way bridge between India and global financial markets.

Inbound Investment – Foreign Capital into India

Inbound funds are investment vehicles set up within GIFT IFSC that channel foreign (non-resident) money into Indian assets. They allow NRIs, OCIs, foreign nationals, and international institutions to participate in India’s equity, debt, and infrastructure markets through a familiar international fund structure – without needing domestic Indian infrastructure.

Who Are Inbound Funds For?

Inbound funds are primarily targeted at investors outside India:

What Do Inbound Funds Invest In?

Inbound funds typically deploy capital into Indian assets such as listed equities, equity mutual funds and ETFs domiciled in India, corporate bonds and government securities, and private equity or venture capital investments. The specific universe depends on the fund category and strategy.

Key Advantages for Inbound Investors:

✅ No FPI License Required: Unlike direct market access, investors can invest through GIFT City funds without needing a Foreign Portfolio Investor registration.

✅ No Indian Bank Account Needed: Capital can be remitted directly from a foreign bank account to the fund’s IFSC account – no NRE/NRO account required in many structures.

✅ USD-Denominated NAV: Fund NAV, subscriptions, and redemptions all happen in USD, eliminating currency conversion friction.

✅ Full Repatriation: Both principal and returns are freely repatriable to the investor’s country of residence with no complex FEMA procedures.

✅ No Income Tax Filing in India: Non-resident investors earning solely from IFSC-based funds are exempt from filing Indian income tax returns.

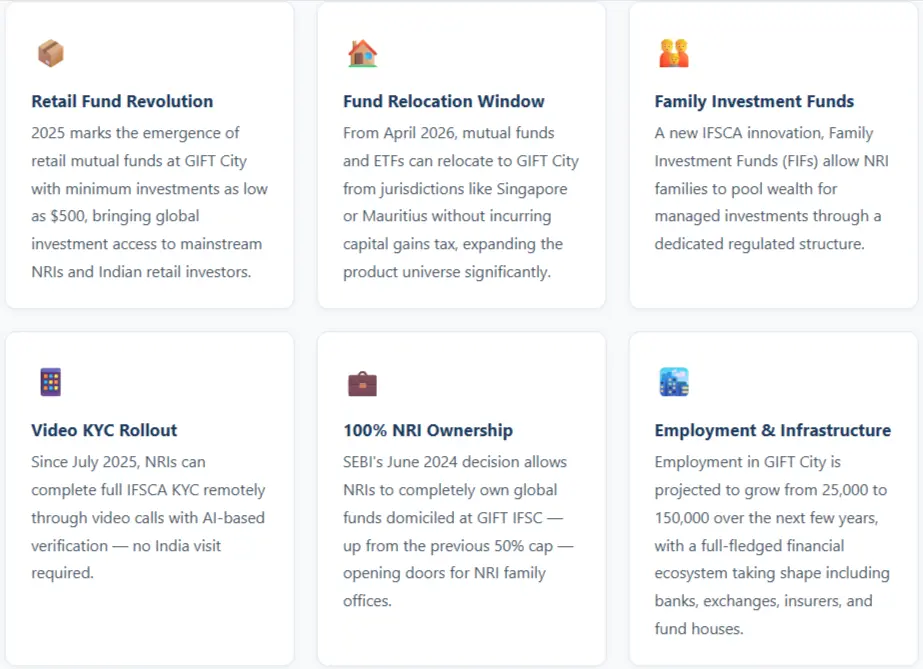

The Retail Milestone: Access for All NRIs

Until mid-2025, GIFT City inbound investment was largely the domain of high-net-worth individuals, with Alternative Investment Funds requiring minimums of $150,000 (subsequently reduced to $75,000). A landmark shift happened in September 2025 when Tata Asset Management launched India’s first retail inbound mutual fund at GIFT City, with a minimum investment of just $500. More AMCs, including Nippon India and Mirae Asset, are following with similar retail offerings, democratising access to India’s growth story for millions of NRIs.

Outbound Investment – Indian Capital into Global Markets

Outbound investment is the opposite flow: capital from Indian entities and individuals invested outside India into overseas assets and markets. GIFT City provides an “onshore-offshore” solution that allows Indian investors to pool capital in USD and deploy it globally through a regulated, compliant framework.

The LRS Route – The Key Entry Point for Residents

Indian resident individuals can invest in GIFT City outbound funds via the Liberalised Remittance Scheme (LRS) under FEMA. The LRS allows each resident individual to remit up to USD 250,000 per financial year for capital account investments – including GIFT City funds. This cap applies annually, making it a renewable channel for building global wealth.

TCS Note: Remittances under LRS exceeding ₹10 lakhs in a financial year are subject to Tax Collection at Source (TCS) at 20%. This TCS is in the nature of advance tax and is adjusted against the investor’s actual tax liability when filing returns. It is not an additional cost but a prepayment of tax.

The OPI Route – For Corporations and Family Offices

Indian companies, trusts, partnerships, and family offices can invest in outbound GIFT City funds via the Overseas Portfolio Investment (OPI) route. Crucially, the OPI route for pooled investments is permitted only through GIFT City-based vehicles, making GIFT IFSC the exclusive gateway for this category of outbound pooled investment. This gives GIFT City outbound funds a significant structural advantage over other offshore alternatives.

What Do Outbound Funds Invest In?

Outbound funds from GIFT City deploy into global assets such as US and global equity ETFs (S&P 500, NASDAQ 100, etc.), international stocks listed on global exchanges, overseas mutual funds and UCITS, global thematic strategies in sectors like AI, semiconductors, and clean energy, and debt or fixed income instruments from global issuers.

Why Outbound via GIFT City vs Direct Foreign Investing?

| Parameter | Direct Overseas Investing | GIFT City Outbound Fund |

|---|---|---|

| Tax Compliance | Investor files capital gains individually per transaction | Tax handled at fund level – simpler ITR filing |

| FX Costs | Per-transaction FX conversion + SWIFT fees | Optimised FX conversion in bulk by fund manager |

| Inheritance / Estate Tax | Potential US estate tax exposure on direct US holdings | No inheritance tax implications through fund structure |

| Minimum Investment | Varies by broker (can be low) | $5,000 for retail funds; $75,000 for AIFs |

| Regulatory Complexity | Multiple forms, disclosures, FEMA reporting | Simplified under IFSCA framework with professional management |

Investment Vehicles Available at GIFT IFSC

GIFT IFSC offers a growing range of investment instruments catering to different risk profiles, investment horizons, and ticket sizes. Here is an overview of the main vehicles:

1. Retail Mutual Funds / Fund of Funds (FoFs)

The newest and most accessible category. These are open-ended schemes regulated under the IFSCA (Fund Management) Regulations, 2025. They can be structured as inbound (investing in Indian mutual funds/ETFs) or outbound (investing in global ETFs and UCITS). Minimum investments start from as low as $500, making GIFT City investment accessible to a much wider audience for the first time.

Retail Funds represent the most significant democratisation of GIFT City – bringing it from an HNI-only zone to a platform accessible by anyone with a few hundred dollars to invest.

2. Alternative Investment Funds (AIFs) – Category III

AIFs are pooled investment vehicles regulated by IFSCA. Category III AIFs, the most common type in GIFT City, employ hedge fund-like strategies and can invest in listed equities, mutual funds, derivatives, and other securities. As of February 2025, the minimum investment was reduced from $150,000 to $75,000 per investor, expanding access for upper-HNI and family office investors. They are typically structured as 3-year closed-ended funds with two-year extension options.

3. Portfolio Management Services (PMS)

PMS offers customised, discretionary portfolio management for high-net-worth individuals who want tailored strategies rather than pooled fund structures. PMS managers at GIFT City can invest in both Indian and global markets, depending on the mandate. Minimum ticket sizes are typically $75,000 – $150,000, and the approach suits investors with specific sectoral views or tailored wealth management needs.

4. Foreign Currency Fixed Deposits

The simplest entry point. Major banks, including HDFC, ICICI, SBI, Kotak, and international banks like HSBC and Standard Chartered, operate IFSC Banking Units in GIFT City and offer USD-denominated fixed deposits. Key features include USD-denominated tenure from 3 months, competitive interest rates of 4.5%-6% per annum, and complete tax-exemption on interest income in India. Minimum investment can be as low as $500.

5. International Stock & ETF Trading at GIFT City

GIFT City hosts two exchanges – NSE IFSC (NSE IX) and India INX. These exchanges list global equities, including Apple, Amazon, Tesla, and more. As of March 2025, NSE IX offers fractional investing in 50 global stocks. Trading hours extend from early morning to early morning IST, covering global market sessions. Investors can access both Indian and global stocks from a single IFSC demat account.

6. USD-Denominated Insurance Products

Several Indian insurers now offer USD-denominated life insurance policies from GIFT City. Policies issued through IFSC insurance offices now offer tax-free proceeds, applicable from April 2025. These products cater to NRIs seeking wealth protection with a life cover component.

| Vehicle | Min. Investment | Best For | Direction |

|---|---|---|---|

| Retail Mutual Fund / FoF | $500 – $5,000 | Retail NRIs, Indian residents via LRS | Inbound Outbound |

| Category III AIF | $75,000 | HNIs, family offices | Inbound Outbound |

| PMS | $75,000+ | HNIs seeking customised mandates | Inbound Outbound |

| IFSC Bank FD | $500 | Conservative investors, NRIs | Banking |

| Stocks / ETFs on NSE IX | Fractional | Active traders, NRIs | Equity |

Who Can Invest & Through Which Route?

| Investor Type | Inbound Funds | Outbound Funds | Annual Limit |

|---|---|---|---|

| NRIs & OCIs | ✅ Eligible (primary audience) | ✅ Eligible | No cap (for NRIs) |

| Indian Resident Individuals | ❌ Not eligible for inbound | ✅ Via LRS route only | $250,000 / year via LRS |

| Indian Corporates, Trusts | ❌ Generally not eligible | ✅ Via OPI route | Up to 50% of net worth |

| Foreign Nationals / Institutions | ✅ Eligible | ✅ Eligible | No cap |

Important for Resident Indians: You can invest in outbound GIFT City funds (those that invest outside India) but you cannot invest in inbound GIFT City funds (those that invest in Indian securities). This is a key FEMA distinction that applies to all resident Indians under the LRS framework.

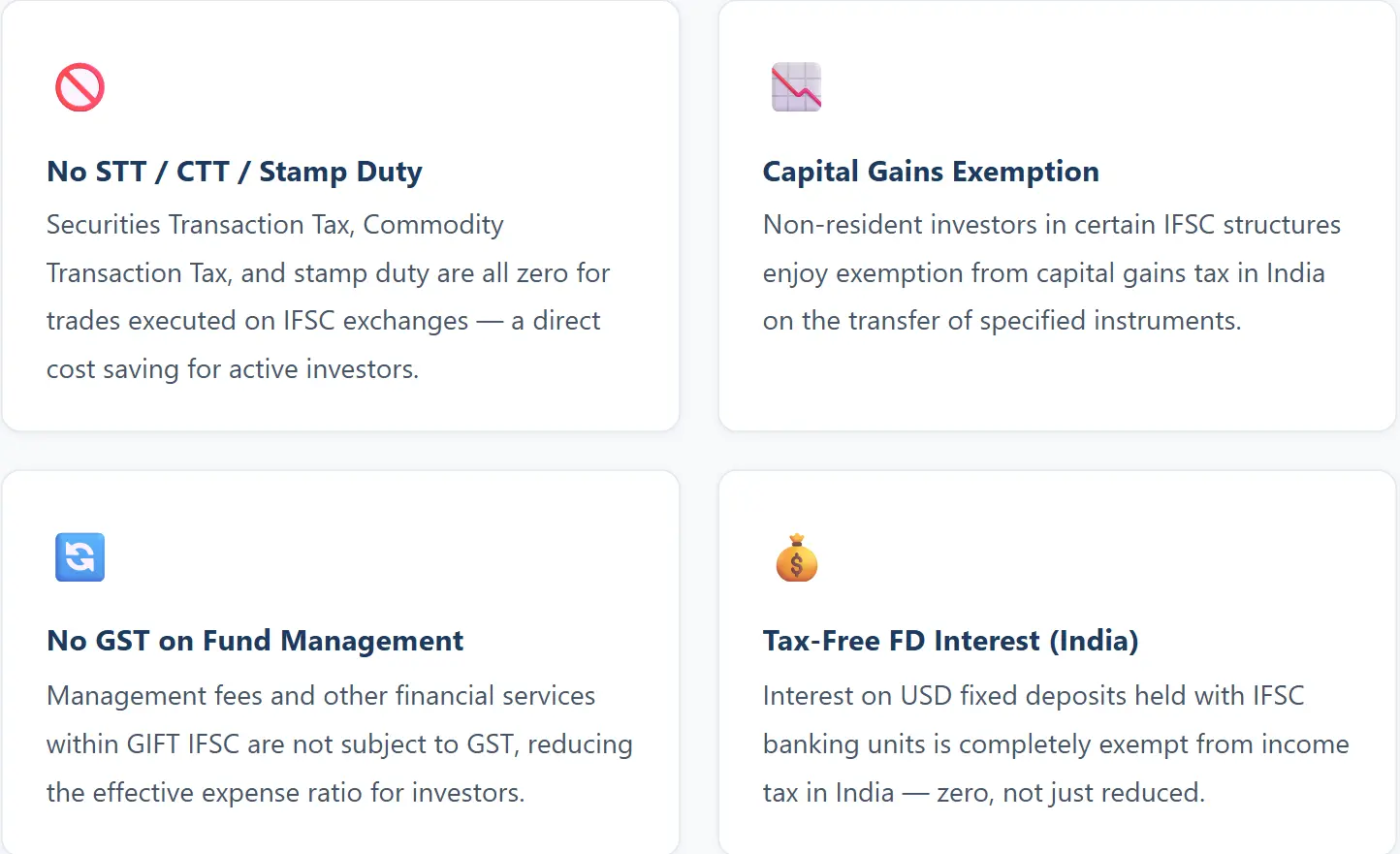

Tax Framework – The Big Advantage

GIFT City’s tax framework is one of its most compelling features. The IFSCA regulatory structure offers a layered set of tax benefits that can be substantially more attractive than investing through domestic or traditional offshore routes.

For Non-Resident (NRI / Foreign) Investors

For Resident Indian Investors (Outbound)

Resident Indians investing in outbound GIFT City funds enjoy key structural benefits over direct overseas investing. Tax is typically paid at the fund level, which simplifies personal tax filing significantly – investors receive post-tax NAV and generally report the investment as a foreign asset in their ITR without having to account for each individual transaction. The fund-level tax approach is especially beneficial when the fund holds foreign equities that would otherwise attract complex foreign asset disclosure requirements.

The 10-Year Tax Holiday for Fund Managers

Fund Management Entities (FMEs) registered with IFSCA benefit from a 10-year income tax holiday on business income. The Budget 2025 extended the deadline for businesses to commence operations and qualify for benefits to March 2030, providing a 5-year window of policy certainty. This incentive keeps expense ratios competitive and attracts top-tier fund managers to set up operations at GIFT City.

Tax-Free Returns for UAE-Based NRIs

NRIs residing in the UAE, Singapore, or other zero-capital-gains-tax jurisdictions get a particularly favourable outcome. Since GIFT City exempts capital gains at the fund level for non-residents, and their country of residence has no capital gains tax either, these investors can potentially receive returns that are completely tax-free. This is a powerful combination that has driven significant NRI interest from the Gulf region.

How to Get Started

The investment process at GIFT City has become significantly more streamlined over the past two years. Here is a generalised flow for both NRI and resident investors:

For NRIs / Foreign Investors (Inbound or Outbound)

1. Confirm Eligibility & Choose Product

Determine your FEMA status as NRI/OCI/foreign national. Choose between retail mutual fund, AIF, PMS, or FD based on investment size and goals.

IFSCA implemented video KYC in July 2025 – remote completion in 15-30 minutes via encrypted video with AI-based face matching. No India visit required. Documents: passport, overseas address proof, bank statement.

For some products, you may need to open an account with an IFSCA-registered bank (HDFC, ICICI, SBI, Kotak, HSBC, Standard Chartered all have IBUs in GIFT City).

Transfer USD (or other foreign currency) directly from your overseas bank account to the fund’s GIFT City IFSC account. No INR conversion needed.

Monitor your investment via the fund manager’s portal. On redemption, proceeds are credited to your IFSC account in USD and fully repatriable to your overseas account.

For Indian Resident Investors (Outbound via LRS)

1. Identify an Outbound Fund / Broker with GIFT City IFSC Entity

Look for fund houses or brokers with an IFSCA-registered GIFT City branch. Major Indian AMCs and brokers like Kotak, Zerodha, and HDFC Securities have IFSC entities.

2. Open a Dedicated IFSC Account

Even if you have a domestic account with a broker, you must open a separate, dedicated IFSC account under their GIFT City entity.

3. Initiate LRS Transfer Through Your Bank

Fill your bank’s LRS remittance form with the purpose code for investment in overseas securities. The bank transfers INR-equivalent funds to your IFSC account in USD. Funds typically reflect in 1–3 working days.

4. Subscribe to the Fund & Monitor

Use the fund manager’s or broker’s GIFT City platform to place the subscription. Track your portfolio in USD. Gains and losses reflect both the underlying asset performance and USD-INR movements.

5. Report in ITR

GIFT City investments are treated as foreign investments for tax purposes. Report them as foreign assets in your annual income tax return (Schedule FA/FSI).

Key Risks & Considerations

Currency Risk: All GIFT City investments are denominated in USD. When you invest as a resident Indian, you convert INR to USD. When you redeem, you convert back. The USD-INR exchange rate introduces an additional layer of return variability – both positive (INR depreciation boosts returns) and negative.

Regulatory Evolution Risk

GIFT City regulations are still evolving rapidly. For example, in 2024, IFSCA prohibited certain US-based ETF investments, disrupting some investor strategies. Tax benefits are currently guaranteed until March 2030 under sunset clauses. The regulatory framework can change, and strategies need to be reviewed periodically.

Tax Complexity for US-Based NRIs

Most GIFT City mutual funds are classified as Passive Foreign Investment Companies (PFICs) under US tax law, which triggers punitive tax treatment for US persons. Additionally, FBAR and FATCA reporting requirements apply when aggregate foreign accounts exceed $10,000. For US-resident NRIs, the tax complications often negate the benefits – specialist cross-border tax advice is essential.

Minimum Investment Barriers

Despite the significant reduction in AIF minimums to $75,000 (from $150,000 earlier), Alternative Investment Funds still require substantial capital that is beyond most retail investors’ LRS budgets. The retail mutual fund category is the solution for smaller investors, but it is still a relatively nascent product category with limited track records.

Market Risk

Like all investments, GIFT City products carry market risk. Inbound funds investing in Indian equities are exposed to Nifty/Sensex volatility. Outbound funds investing in global equities are exposed to global market risks, including geopolitical events, US Fed rate changes, and sector-specific corrections.

The Evolving GIFT City Ecosystem

GIFT City in 2025 is not the same ecosystem it was in 2022 or even 2024. The pace of regulatory evolution and product launches has accelerated significantly. Here are the key developments shaping the GIFT City investment landscape:

The Big Picture: India represents roughly 4% of global market capitalisation today, yet is projected to become the world’s third-largest economy in the next decade. GIFT City is being architected as the conduit that connects this growth story with global capital – and enables Indian savers to participate in global markets with the same ease that investors in Singapore or Hong Kong have long enjoyed. The regulatory, tax, and infrastructure buildout happening at GIFT City right now is setting the foundation for what could be one of the most significant financial ecosystems in Asia over the next two decades.

Disclaimer: This blog is for informational purposes only and does not constitute investment or financial advice. Investments carry risk, including loss of capital. Tax laws and regulations may change. Please consult a qualified financial, tax, or legal advisor before investing.